Advok8 Strategic Brief October 2020, Part 1

By Steve A. Day, President of Advok8, ©Coypright 2020, Advok8

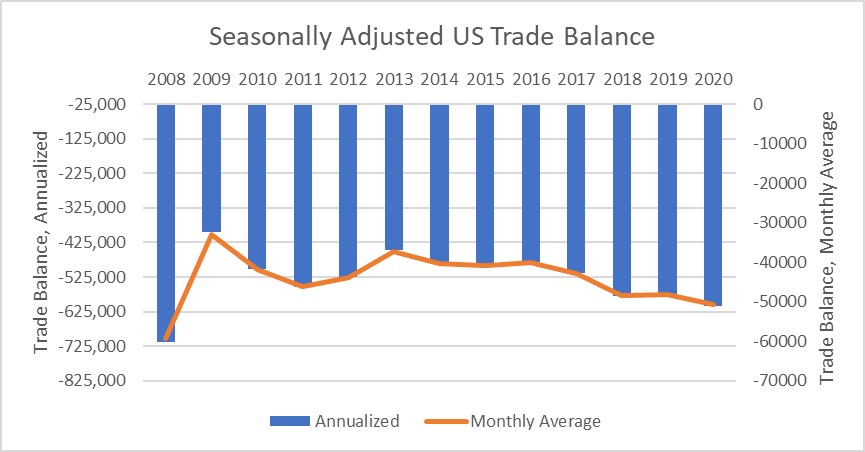

The economic recovery over the next two or three years will be the most important goals for most multi-national companies that are trying to recast their existing strategies based upon a new reality. The easy answer is to exclaim that our misfortunes are all related to COVID impact. However, that is not the case. The first thing we will examine is that continued worsening of the US trade balance. Since 2016, it has increasingly worsened. US Exports were dropping and are also projected not to recover. As the US trade embargo and other Diplomatic actions have hurt trade around the world, countries are building global supply lines to circumvent the United States. In doing so, we will see roughly 17% permanent fall-out that will continue (all other things equal).

Figure 1. US Census Bureau Trade Analysis ($ millions)

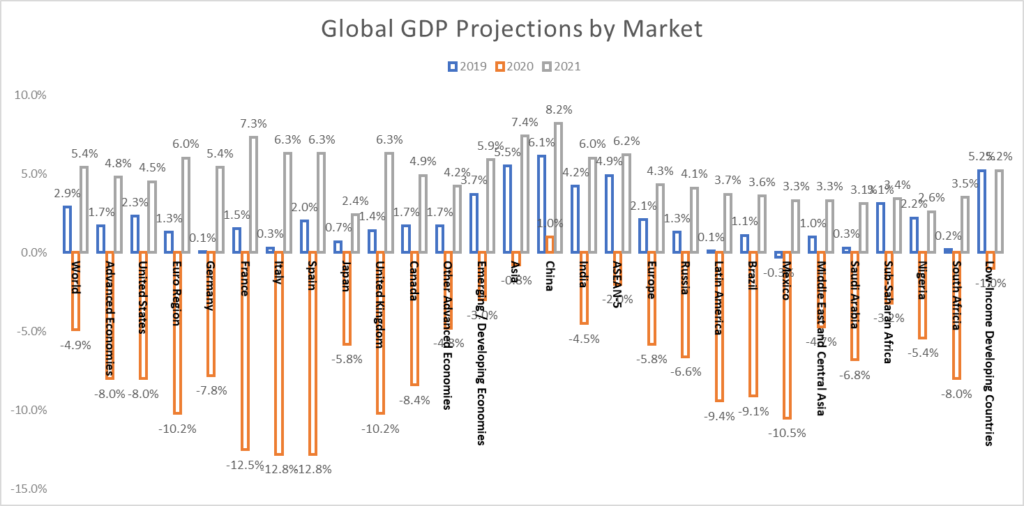

To understand the before and after within the United States, the seasonally adjusted GDP in 2019, projected 2020 and projected 2021 will be 2.3%, MINUS 8.0% and 4.5% annually. This aggregate for the Global economy for the same period is 2.9%, MINUS 4.9% and 5.4%. The aggregate for comparable advanced economies is 1.7%, MINUS 8.0% and 4.8%, respectively.

The United States was already in a slight decline before COVID. This was similar to other established economies, at 2.3% GDP growth. The problem was that COVID hit the United States with a greater economic impact than many competitive countries. All other things equal, the projection is that almost all of our competitive economies will recover in 2021 at a much greater rate than the United States. As compared to our recovery in 2021 projected at 4.8%, Asia will recover at a percent of 7.2%. Europe will recover at a percent of 6.0%. Low income countries will recover at a rate of 5.2%.

These two specific issues are related to each other. The United States was already in a decline of exports and an increase of trade imbalance, before COVID. As the World contracted, the recovery will already have been seeded with non-United States global supply chains. Agricultural products and Steel have both been front and center for the last few years, as other countries have built up their industries to bypass US tariffs on their goods.

Figure 2. International Monetary Fund World Economic Projections

It is clear from Figure 2 that the countries having the most difficult time with COVID are also the countries that have experienced some of the greatest recessions. These include the United States, Italy, United Kingdome and Mexico. It should be noted that the chart also hides countries that delayed testing and response. India will have one of the latest impacts, as they are just starting to feel the massive scale impact of the COVID plague.

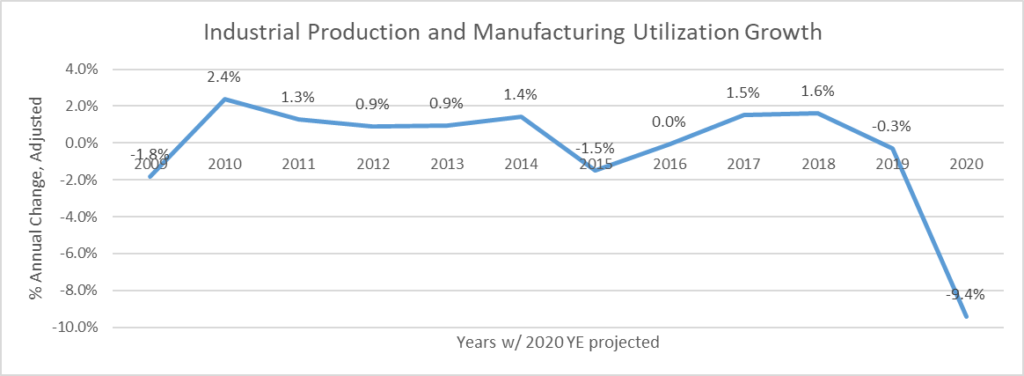

Figure 3. US Federal Reserve Estimates of Industrial Production Growth

The final aspect of the US economic problem is within industrial production. After the 2008 recession, the industrial production had begun to heal itself. 2010, for instance, reflected 2.4% growth. In fact, 2011, 2012, 2013, 2014, 2017 and 2018 all were very productive US manufacturing years. However, even before the COVID hit the United States, we were experiencing a deceleration of industrial production in 2018, 2019 and then 2020. This was caused by three things.

- The North American Free Trade Agreement (NAFTA) and the Trans-Pacific Partnership (TPP) free trade deals ensnared 15 countries in a race to the bottom, as major corporations began to move their manufacturing facilities to the locations with the lowest cost of labor … even locations with histories of child labor.

- United States tariff wars with China and other countries on key goods have been escalating since

2016. This has had a double-edged sword on the economy. Based on 2019 import levels, U.S. and retaliatory tariffs currently impact over $460 billion of imports and exports, and tariffs are increasing annual consumer costs by roughly $57 billion annually. (Source: The American Action Forum, US Federal Reserve).

With this situation, the United States may be facing a very tough road for the next five years in attempting to recover three vital aspects of the economy. Manufactured Goods. Exports. Import dependent goods and services.

How will politicians and financial institutions react to this? The most likely way is to stimulate the economy in sectors that do not heavily rely on these three attributes of the economy. This will lead to four parts of the economy that will be important, if economic recovery is the goal:

- Health care and pharmaceutical products and services.

o Provided that COVID vaccine and COVID therapies are homegrown.

- National, state and municipal infrastructure and technology projects.

- National residential investment and green energy delivery

- Stimulation of consumer spending

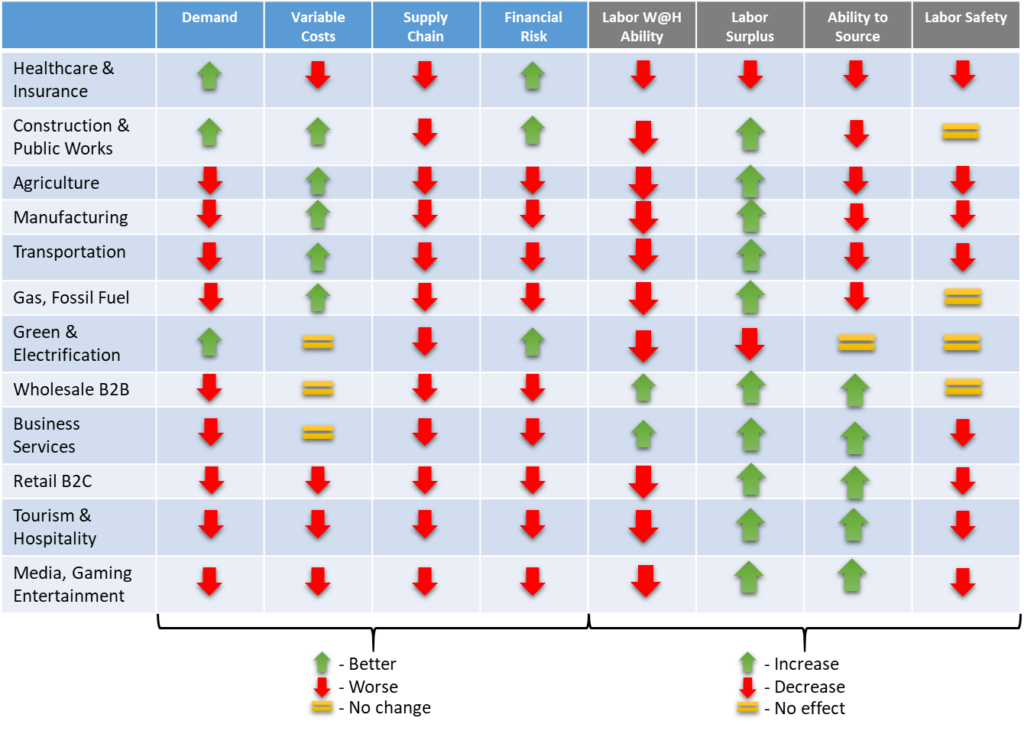

With this said, the business sectors will all have a different reaction to COVID and the future of recovery. It is determined by two sets of variables. The first set our four business conditions. Demand for product, projected variable costs, global supply chain and the financial risk attached to this line of business. The second set of four business conditions will involve the re-acquisition of labor after COVID related job loss, the worst job loss period in the history of the United States.

Figure 4. Derived from IMF Blog, McKinsey and S&P Global

Demand for Goods and Services

There are only three segments of the economy that are projected to have a high demand. Healthcare products and services will continue to be in high demand. Most experts agree COVID recovery will take until at least the end of 2021. Just to finish off healthcare, it is going to be a double edge sword. Huge demand for healthcare is tempered with all other aspects of the business sector being bad. Costs are escalating. Labor will be harder and harder to find. Safety is going to continue to be a significant problem.

Construction and public works were addressed above. Residential, Commercial, and public works projects are being projected to take on a significantly higher percentage of the GDP. Consider that exports have significantly dropped off. As pointed out in the chart, imports or supply chain have been irreversibly damaged by tariffs and other global conflicts (withdrawal from trade associations and exit from other international stimulus bodies). Therefore, it is logically forecasted that homegrown production has to pick up the slack. This is why demand is increasing in these areas. And as a side note, the United States has always led the world in innovation and technology. The only place where this is actively possible in our business sectors is in green energy and electrification.

Variable Costs

Variable costs are interesting. The low cost and high access to oil has allowed most industries to enjoy a reduction in variable costs and transport costs. This has been seen as a positive in most industries. Furthermore, the labor wages and benefits have remained equal, and in most cases, actually decline relative to the spending power of the consumer. Considering our spending power is in decline, real wages have decreased more substantially. Therefore, most industries have experienced an improvement in variable costs. COVID has created massive layoffs and furloughs. This again has allowed Industries to cut labor costs and benefit costs.

Going into the future, it is hard to gauge the number of people that will be rehired. And as in every other point of the recession, the actual increase of wages and benefits are typically stalled. Some experts have suggested that only 50% to 67% of the workers displaced will actually be hired again.

Supply Chain Issues

Simply put, the global supply chains were destroyed by the tariffs that began in 2016 and have continued to be multiplied to this very day. The World Economic Forum states “Tariffs are now [2017] imposed on over $275 billion of US imports, mostly from China, but also Japan, South Korea, Canada, and Mexico (Chudik 2019, Fajgelbaum et al. 2019), while the US’ trading partners have retaliated with approximately $121 billion in tariffs on US goods (Amiti et al. 2019).” This represents a total of $396 billion dollars of impact.

Antidotally, Advok8 was tasked by a client to examine global supply chain impacts across various materials and components. What was apparent is that foreign, tariffed manufactures and suppliers were building new relationships with other countries to sell their products. They tore down their US global supply chains and rebuilt new ones with companies (even US companies) to destinations other than the United States.

Rebuilding manufacturing within the United States, or enabling US companies to sell exports globally, will be very difficult and take years to rebuild the relationships and global supply chains.

Financial Risks by Industry

The Brookings Institute has done a study on the Industry segments that will be most and least impacted by COVID and the impending recovery. The bad news is that there are not allot of Industries that will be positively impacted. There is also a different outcome based upon the Presidential election and the 2021 makeup of the senate. These two things drive healthcare, insurance, public works and several other industries.

Republican response will be to tear apart healthcare, favor large healthcare technology companies and provide substantial financial aid to large corporations. Democratic response will be to preserve healthcare, favor low cost delivery of technology, minimize financial aid to legacy industries and transform towards more progressive public works, green energy and electrification.

The most probable projection is that healthcare & insurance, construction & public works, and green energy & electrification will be in growth modes. All remaining industries will be in decline, or remaining in recovery mode. The industries that are most likely to fail will be Retail B2C, tourism & hospitality, and media, gaming & entertainment.

COVID Impact on Labor and Recovery

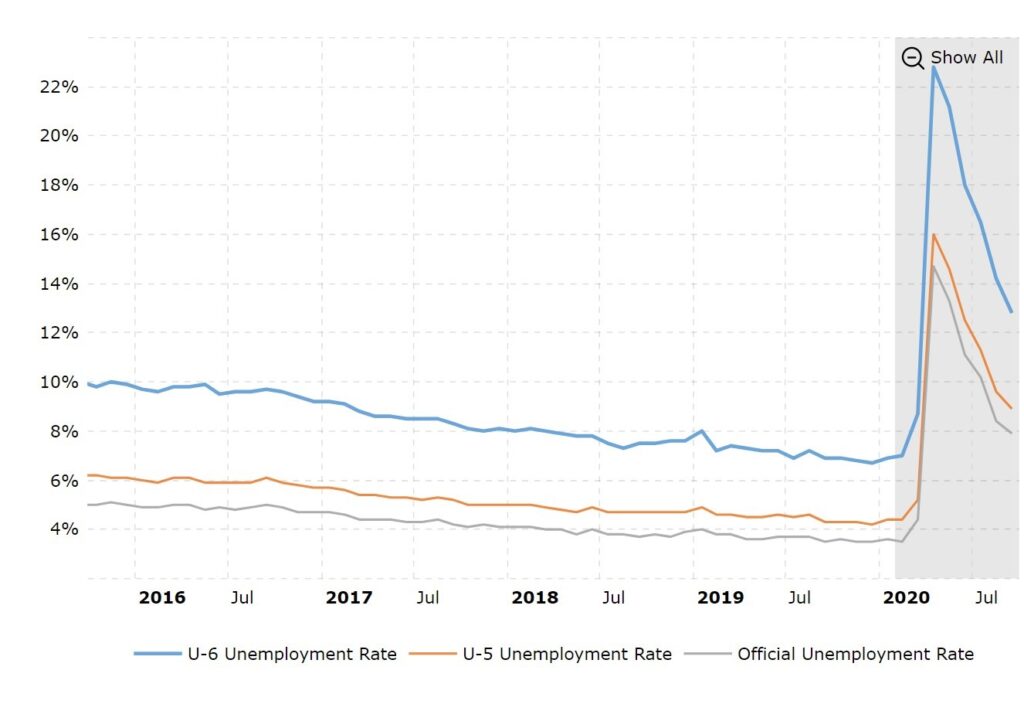

As of July, 2020, 22 million jobs had been lost and only 9 million had been rehired. Two months later, it was reported that 39 people were seeking work related, public financial assistance. Figure 5 reflects this with a September U-3 unemployment rate of 7.9%. However, the U5 and U6 unemployment rates are even more troubling, as they sit at 8.9% and 12.8% respectively. These are more important because they tell a story of people leaving the workforce, semi-permanently.

What has happened within 2020 is that the declining US labor participation rate exploded. Many of these people were reaching different stages of their lives.

• The U-6 rate is the unemployment rate that includes discouraged workers no longer seeking jobs and part-time workers seeking full-time employment. In addition to the marginally attached category, the U-6 rate also includes the underemployed in the labor force in its metrics. [Wiki]

• The U-5 rate is the total unemployed, plus discouraged workers, plus all other marginally attached workers, as a percent of the civilian labor force plus all marginally

In looking at this, we are seeing a job participation rate in the United States falling from 70% to 60%. Essentially 10% of the workers are opting to leave the workforce. These people are often the most qualified and most senior workers. H1 visa workers are moving to other countries. Canada, for instance, is seeing a large spike in these people immigrating since 2016. Foreign workers are simply changing their destinations to other countries. Secondly, the baby boomer generation of worker is not only naturally retiring but is also opting to retire early. Third, union and other skilled craftsman have been discouraged for years from the workplace. They also are tending to migrate towards a gig economy.

This impact the United States economy with respect to all facets of the performance. Capacity, productivity, labor supply, tax revenue and a wide range of positive stimuli in the economy will downturn.

As always, the labor market will return. However, the return often masks quality, competence and replacement costs that are steep for United States manufacturing and B2B organizations, particularly.

Conclusion

As Advok8 works with our customers, we are constantly looking for the opportunities to reform and refocus. It is important to understand that customers are always changing. Products and services are always changing. While this is a very broad study, we specialize in drilling into any organization to find the details associated with the future growth and strengths.

Often, our clients have an internal view. The strategy within the walls. Our goal is to getting our clients to literally think outside the box. Find those opportunities that are still in the future and still unspoken for. This critical thinking often can only come from those that are on the outside looking in.

Leave a Reply